Fed FOMC Meeting Is Approaching, Where Is the Focus? Will There Be Further Rate Cuts This Year?

The Federal Reserve is expected to hold interest rates steady at its April meeting, with market consensus at 100% probability. The focus shifts to Chairman Powell's press conference amid geopolitical tensions and oil price shocks impacting headline inflation. Core inflation remains stable, suggesting a "hot headline, cool core" scenario. With an anticipated leadership transition to Kevin Warsh, who exhibits a dovish tilt, market expectations for future rate cuts show significant divergence. Uncertainty surrounding energy shock duration and the new chair's influence leaves the Fed's policy path layered with unknowns.

TradingKey - Global financial markets are bracing for a "Super Central Bank Week" this week, with five major central banks, including the Federal Reserve, the European Central Bank, and the Bank of Japan, set to release interest rate decisions in rapid succession.

For the Federal Reserve, the April policy decision to be announced on April 29 ET will face market scrutiny against an increasingly complex macroeconomic backdrop: tensions in the Middle East remain volatile and uncertain, oil price shocks are beginning to filter through to core inflation, and the U.S. Treasury market is already "pricing in" the profile and outlook for Chairman Powell, whose leadership transition is slated for next year.

What are the key focus areas for the April FOMC?

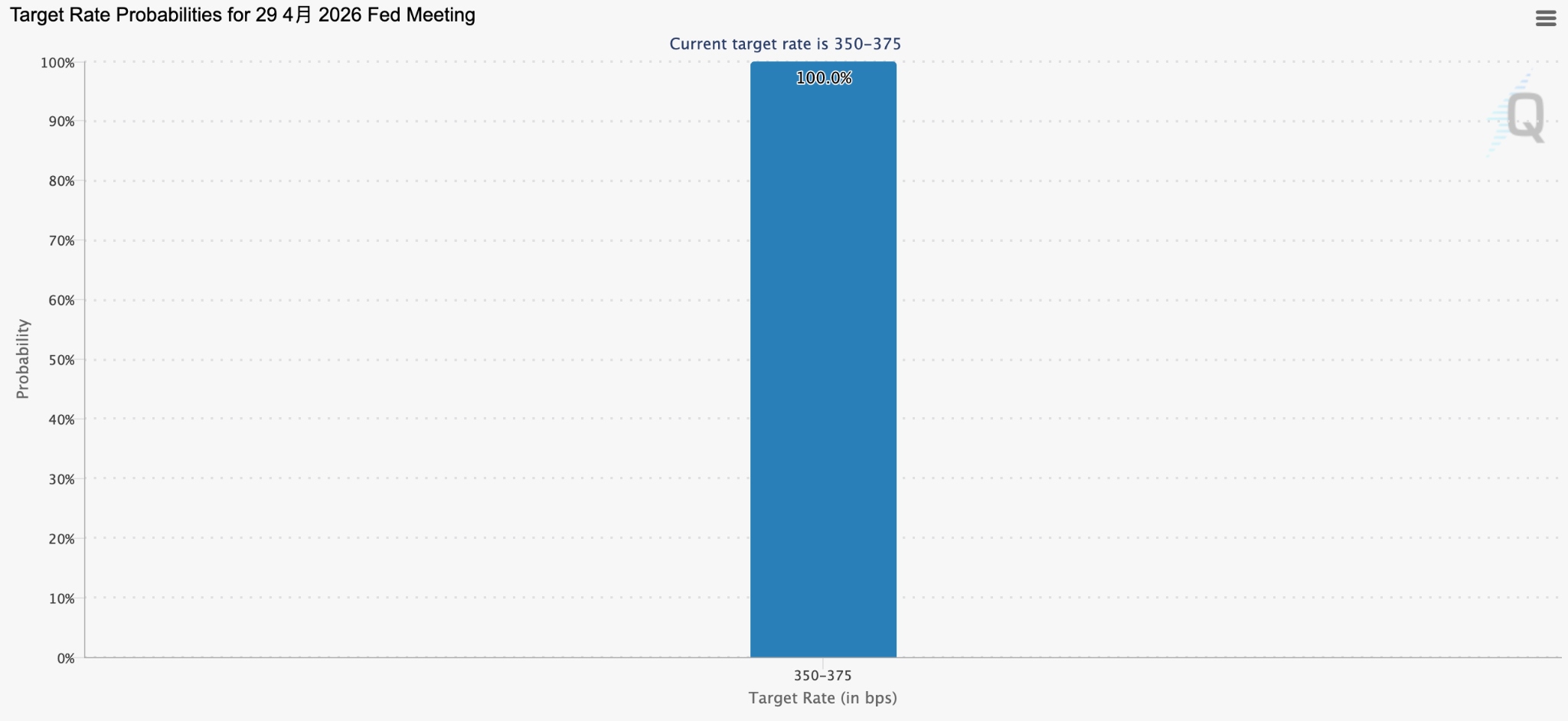

The interest rate decision itself holds little suspense. CME FedWatch data shows that market pricing reflects a 100% consensus probability that the Federal Reserve will keep interest rates unchanged in April.

[Probability of a Rate Cut in April, Source: FedWatch]

Since the March meeting, Fed officials have mostly adopted a wait-and-see stance. Financial markets are currently pricing in less than one rate cut for 2026. Powell is expected to continue emphasizing the uncertainties facing policy, and interest rates are anticipated to remain unchanged at the April meeting.

The real focus lies in the unique structural factors of this release. This meeting marks Jerome Powell's final official FOMC meeting as Chair and will likely be the last press conference of his term.

Markets widely expect the Senate Banking Committee's vote on Kevin Warsh, Donald Trump's nominee for Fed Chair, to take place on the evening of April 29, Beijing time. If confirmed, Warsh will officially succeed Powell in May.

Warsh's testimony was largely consistent with previous remarks. His focus on trimmed-mean inflation indicates a continued desire to push for rate cuts, advocating for a dual path of "quantitative tightening and rate cuts." Although he made no explicit commitments regarding interest rates, his rhetoric already exhibits a clear dovish tilt.

When the results of this policy meeting are released, the most anticipated highlight will likely be Powell's remarks during the press conference.

Observers are closely watching whether Powell will use a clearer signal toward a rate-cut path as a prelude to handing over the reins to Warsh.

Meanwhile, traders are highly focused on the fact that this meeting includes no updated dot plot or economic projections, meaning the only incremental information available for analysts and traders to dissect will be the wording of Powell's press conference.

Christian Scherrmann, Chief US Economist at DWS, noted in a recent preview that inflation resulting from the conflict in Iran has begun to manifest in economic data. In March, headline CPI jumped nearly one percentage point year-over-year to 3.3%, while consumer confidence simultaneously plunged to historical lows.

However, core inflation has yet to show significant pass-through from energy prices, and long-term inflation expectations remain stable. This "hot headline, warm core" scenario aligns perfectly with the Federal Reserve's textbook response logic: staying on hold while tilting rhetoric toward the hawkish side.

Chicago Fed President Austan Goolsbee, a voting member of the FOMC, warned as early as April 7 of a worst-case scenario: inflationary pressure from high oil prices combined with persistent tariff effects could cause American consumers to lose confidence entirely, leading to a stagflationary recession.

However, with the inflation data verification window still open, the Fed is unlikely to take a decisive step in its stance. Behind the consensus of holding rates steady in the short term, Wall Street's forecasts for the Fed's mid-term trajectory show unprecedented divergence.

Michael Feroli, Chief US Economist at J.P. Morgan, believes the Fed will keep rates unchanged for the remainder of 2026, with a potential 25-basis-point hike not occurring until the third quarter of 2027. Conversely, Bank of America still expects the Fed to cut rates twice this year.

Will there be further rate cuts this year?

Current rate cut probabilities have been positioned within an extremely delicate neutral range by bilateral market pricing; while a cut remains possible, the timing of the initial move is highly likely to be delayed.

A Reuters survey conducted from April 17 to 21, covering 103 economists, showed that 71 expect at least one rate cut this year, with the median forecast calling for a single cut—consistent with the dot plot released by the Federal Reserve last month. However, nearly one-third of economists expect the Fed to keep rates unchanged for the entire year, a proportion that has nearly doubled since the previous survey.

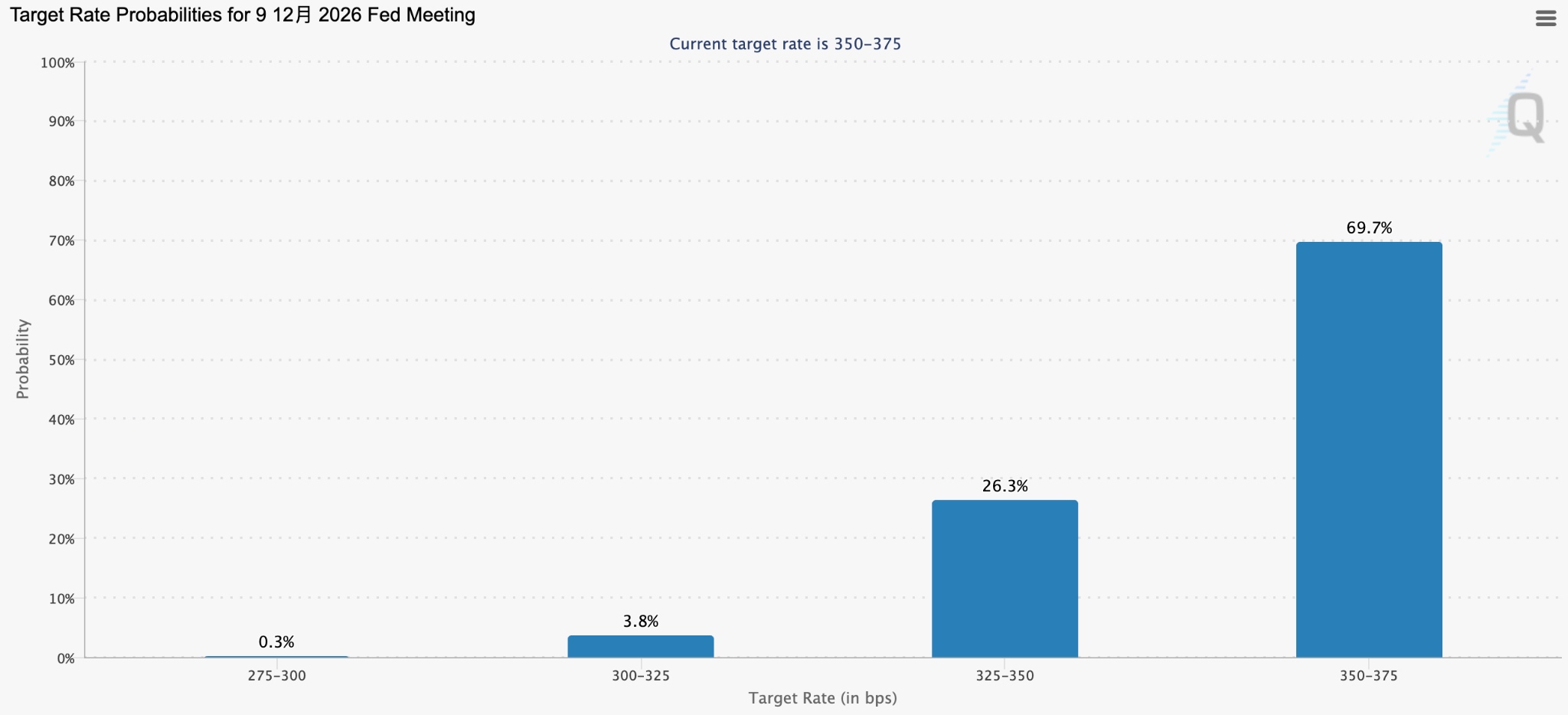

On one hand, the duration of the energy shock remains the greatest unknown. LSEG data shows that markets expect less than one standard 25-basis-point rate cut by December, whereas at least two cuts were anticipated prior to the outbreak of the conflict between the U.S. and Iran.

Some analysts also point out that even if oil price gains slow, overall prices remain elevated, making a near-term rate cut inappropriate; the FedWatch tool also indicates a nearly 70% probability that rates will remain unchanged through the end of the year.

[Probability of rate cuts in December 2026, Source: Fed Watch]

In its March FOMC statement, the Federal Reserve explicitly stated that "uncertainty exists regarding the impact of the Middle East situation on the U.S. economy."

On the other hand, the transition in Federal Reserve leadership is injecting new variables into the rate-cut narrative. Kumar, a global economist at Jefferies, believes a Fed led by Warsh would be more "dovish" regarding interest rates, predicting two cuts this year.

However, Deutsche Bank economists warn that Warsh is just a single policymaker; even if he advocates for rapid rate cuts, he would still need to persuade the policy committee and would require time after taking office to build trust and credibility within the board.

Barclays' analysis serves as a median reference for Wall Street: against a backdrop of widespread uncertainty regarding inflation trends, the Fed is likely to adopt a wait-and-see approach; should inflation recede as expected, the Fed will gain sufficient confidence to begin easing policy around September.

From data points to official rhetoric and the leadership transition, the Federal Reserve's future path is compounded by multiple unknown variables beyond the established ones. The fate of transit through the Strait of Hormuz may ultimately drive a turning point for global inflation, while the new chair taking office in May will define the dovish or hawkish leanings of the Fed for the next economic cycle.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles