China Policy Outlook: Will It Continue Its Easing Strategy in 2025?

TradingKey - Global stock markets have climbed higher in 2024 and most investors will no doubt be happy with their returns had they stayed invested.

One big market that has rebounded more recently has been China, with the MSCI China Index having gained 16.5% so far this year (as of 29 November 2024).

A lot of the more positive sentiment has been related to stimulus measures that Chinese policymakers are taking to help shore up the world’s second-largest economy.

So, what has been done so far in 2024 and what’s the policy outlook for 2025? Will investors see continued easing on both the monetary and fiscal policy fronts?

Policymakers face challenges with slowing Chinese economy

Like all economies, in China, there are two policy levers that can be pulled to help spur growth; monetary and fiscal. Monetary policy refers to central bank’s interest rate levels and the supply of money into the economy – this part is dealt with by the People’s Bank of China (PBOC).

On the fiscal side of things, this is spending by the government that can help encourage capital to flow into certain parts of the economy. So far in 2024, China’s economy has been suffering from weak consumer sentiment and slowing growth.

In Q3 2024, China’s GDP growth slowed to 4.6% year-on-year, down from the 4.7% year-on-year growth that was recorded for Q2 2024. The Q3 growth number turned out to be the lowest growth figure in six quarters. Furthermore, while falling prices (or deflation) has been reversed, inflation in the Chinese economy is still worryingly low.

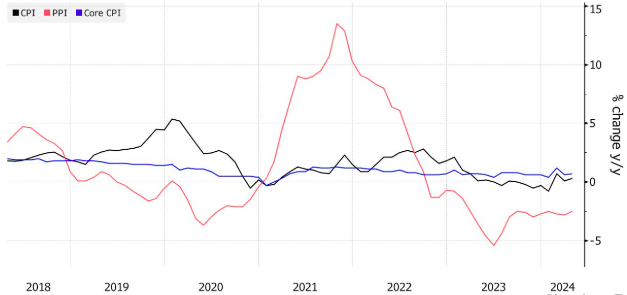

China’s consumer inflation remains tepid while PPI in negative territory

Source: National Bureau of Statistics, Bloomberg

For November 2024, China’s consumer price inflation (CPI) fell to a five-month low with prices climbing just 0.2% year-on-year. Meanwhile, China has deflation in the producer segment with the producer price index (PPI) seeing prices fall for the 26th consecutive month in November.

September announcements turbocharge stock markets

All this had spurred policymakers to act. In late September, the PBOC announced a series of measures that helped lift sentiment. It was also no coincidence that the first announcement came only a day or two after the US Federal Reserve (Fed) announced its first interest rate cut in over four years.

On 24 September 2024, the PBOC revealed that it would set up a RMB 800 billion (US$110 billion) swap facility for securities brokers and insurers. This fund would allow them to tap funds to purchase equities in onshore Chinese stock markets.

Only a day after that announcement, the PBOC also cut its medium-term lending facility by 30 basis points (bps) to 2%. That was the biggest cut to the rate since 2016 and this facility is typically used by the Chinese central bank to help guide market interest rates for the broader economy.

Beyond that, another reserve requirement ratio (RRR) cut was implemented – a favourite tool of policymakers in China. This allowed another RMB 1 trillion in long-term funds to be freed up for bank lending, boosting capital for the economy.

Chinese stocks rallied hard on this announcement and the broader market was up by anywhere from 20% to 25% from the pre-announcement levels.

Policy outlook for 2025 looks promising

Of course, investors will be looking to how fiscal policy now plays out given the PBOC has done so much in such a short space of time. Currently, the China annual Central Economic Work Conference (CEWC) is taking place – 11-12 December – and a raft of measures are starting to emerge.

There are expectations that specific policy measures, related to boosting consumption, would be unveiled during the conference. This is a welcome announcement given that the Politburo held a meeting on Monday (9 December) and said that it would adopt a “more active set of policies” that would look to combine with “moderately loose” monetary policy.

This would be done to expand domestic demand in 2025 and stabilise both the stock and property markets in China. In November, the central government unveiled an additional RMB 6 trillion bond quota to help resolve local government debt and said it would implement more “forceful” measures to help underpin China’s growth.

What that looks like could involve heavier spending on the fiscal front to boost consumer sentiment. However, for investors, only more specific details from the CEWC will be likely in March 2025 when the National People’s Congress takes place.

However, with tariffs likely on the agenda when Trump becomes US President again in early 2025, policymakers in China are looking to keep some “dry powder” for stimulus next year. That could indeed see the government unveil meaningfully more powerful stimulus for its domestic economy to drive increased consumption.