อัตราผลตอบแทนพันธบัตรรัฐบาลที่เพิ่มขึ้นถือเป็นความท้าทายที่ใหญ่ที่สุดต่อตลาดกระทิงของทรัมป์

นักลงทุนใน Wall Street หวังว่างาน Santa Rally แบบดั้งเดิมจะปิดตัวลงในปีนี้ แต่ก็ยังรู้สึกผิดหวัง ฟิวเจอร์สดัชนีหุ้นแนะนำให้มีการต่อสู้ดิ้นรนอย่างต่อเนื่องเพื่อตลาดหุ้น หลังจากดัชนี S&P 500 ลดลง 1.1% เมื่อปลายสัปดาห์ที่แล้ว

ตามที่นักเศรษฐศาสตร์ระบุว่า ปี 2024 ถือเป็นปีแห่งการสร้างสถิติของวอลล์สตรีท S&P 500 ขึ้นไปแตะระดับสูงสุดเป็นประวัติการณ์ที่ 57 จัดให้อยู่ในห้าปีแรกสำหรับสถิติสูงสุดตลอดกาล ในปีที่ผ่านมา Nasdaq Composite เพิ่มขึ้นมากกว่า 31% S&P 500 เพิ่มขึ้น 25% และค่าเฉลี่ยอุตสาหกรรม Dow Jones เพิ่มขึ้น เพียงเล็กน้อย 14%

อย่างไรก็ตาม อัตราผลตอบแทนพันธบัตรที่เพิ่มขึ้นกำลังสร้างความท้าทายให้กับตลาดหุ้น อัตราผลตอบแทนพันธบัตรรัฐบาลอายุ 10 ปีปิดตัวเมื่อสัปดาห์ที่แล้วที่ระดับสูงสุดในรอบเจ็ดเดือน ตั้งแต่เดือนกันยายน อัตราผลตอบแทนได้เพิ่มขึ้นเกือบร้อยละเต็ม แม้ว่าธนาคารกลางสหรัฐจะปรับลดอัตราดอกเบี้ยอ้างอิงแล้วก็ตาม

อัตราผลตอบแทนพันธบัตรอาจกดดันหุ้นได้

นักวิเคราะห์ มองว่า อัตราผลตอบแทนพันธบัตรที่เพิ่มขึ้นนั้นเกิดจากความกังวลเกี่ยวกับนโยบายภาษีและนโยบายภาษีของประธานาธิบดีโดนัลด์ dent รัมป์ นโยบายเหล่านี้สามารถกระตุ้นอัตราเงินเฟ้อและขยาย defi ของรัฐบาลกลาง เพิ่มอุปทานพันธบัตร และราคาที่กดลง

Julian Emanuel นักยุทธศาสตร์ของ Evercore ISI เตือนว่าอัตราผลตอบแทนระยะยาวอาจยังคงสร้างแรงกดดันต่อหุ้นในระยะกลางต่อไป แม้ว่าสภาพเศรษฐกิจในวงกว้างจะยังคงเอื้ออำนวยก็ตาม

“ อัตราผลตอบแทนพันธบัตรระยะยาวที่เพิ่มขึ้นถือเป็นความท้าทายที่ใหญ่ที่สุดต่อตลาดกระทิงเมื่อเริ่มต้นปี 2568 ” เอ็มมานูเอลเขียนในบันทึกล่าสุด โดยชี้ไปที่ความผันผวนของตลาดทุนที่เพิ่มขึ้นหลังจากการประชุมของธนาคารกลางสหรัฐในเดือนธันวาคม

ตลาดตราสารหนี้กำลังถึงจุดสูงสุดในขณะที่ตลาดน้ำมันดิบพบจุดต่ำสุด ซึ่งทั้งสองอย่างได้รับแรงหนุนจากอัตราเงินเฟ้อเป็นส่วนใหญ่ Bitcoin วางตำแหน่งตัวเองเป็นผู้เล่นหลักเนื่องจากมีการกระจายอำนาจและมีอุปทานที่จำกัด ซึ่งเป็นทางเลือกแทนการเสื่อมราคาของสินทรัพย์แบบเดิม เช่น…

— GG (@LuillyDRR) 27 ธันวาคม 2024

Emanuel emphasized that while bond yields may pull back slightly in the short term due to elevated Treasury short positions and easing geopolitical tensions, the medium-term outlook remains challenging. The interplay between rising bond yields and equity valuations will be crucial in determining market trends in early 2025.

The strategist also predicts that a 10-year Treasury yield of 4.5% is manageable for equities, but a breach of 4.75% could trigger a deeper correction. Notably, stocks have shown resilience in periods of rising yields, advancing 117% since the bond market trough in 2020.

However, during periods when yields surpassed 4.5% or 4.75%, equities posted negative returns of -2.1% and -3.7%, respectively.

Corporate earnings bolstered by economic resilience

In 2024, earnings growth extended beyond the “Magnificent Seven” tech giants, with the other 493 S&P 500 companies exiting their earnings recession. According to FactSet data, S&P 500 earnings are projected to grow 15% year over year in 2025.

Keith Lerner, co-chief investment officer at Truist, notes that this earnings growth will likely sustain the bull market. “The weight of evidence suggests the primary market trend remains higher, driven by earnings growth in 2025,” Lerner stated in his market outlook.

The broader U.S. economy has also demonstrated resilience. November retail sales exceeded expectations, GDP growth remains above trend at 3%, and the unemployment rate continues to hover around 4%. While still elevated, inflation has shown signs of moderation, giving investors hope for a “soft landing” where prices stabilize without significant job losses.

Market tailwinds and headwinds into 2025

Several tailwinds are supporting market optimism heading into 2025. Record corporate profits are expected for a second consecutive year, with net profit margins projected to remain nearly 12%. Sectors beyond technology, including health care, industrials, and materials, are anticipated to see profit increases in the high teens.

However, headwinds are where economists are expressing little to no optimism. Federal Reserve officials now project the federal funds rate to fall to 3.9% in 2025, an increase from their earlier September estimate of 3.4%.

While the Fed delivered a substantial 50 basis point rate cut in September, most adjustments over the past year have been in smaller 25 basis point increments. The latest projections suggest the central bank anticipates two more rate cuts in 2025, down from the four cuts previously forecast in September.

BREAKING: Fed projections imply 50 basis points of rate cuts in 2025, another 50 bps in 2026.

— unusual_whales (@unusual_whales) December 18, 2024

If interest rates are not accordingly cut in 2025, given the Federal Reserve’s commitment to combating inflation, it may risk a policy error that could potentially harm the labor market.

Additionally, analysts reckon that the Trump administration’s policies, while business-friendly, could introduce growth challenges through higher tariffs.

Tech stocks, which have driven much of the market’s gains, face potential stagnation as investors grow wary of excessive spending on artificial intelligence without corresponding earnings growth. While a collapse in tech valuations is unlikely, a moderation in valuations could shift investor focus toward undervalued sectors like health care and materials.

From Zero to Web3 Pro: Your 90-Day Career Launch Plan

บทความที่เกี่ยวข้อง

สิ่งที่คาดหวังจาก Eli Lilly ในปี 2026? หุ้น LLY ยังเป็นโอกาสในการเข้าซื้อที่ดีหรือไม่ในขณะนี้?

เป้าหมายและจุดมุ่งหมายหลักของบริษัทในปี 2026 คือการรักษาตำแหน่งผู้นำในด้านการจัดการน้ำหนัก พร้อมกับการขยายธุรกิจไปยังกลุ่มการรักษาโรคด้านอื่น ๆ เพิ่มเติม เพื่อให้การเติบโตของรายได้ไม่ต้องพึ่งพาผลิตภัณฑ์เพียงชนิดเดียว ทั้งนี้ คาดการณ์ว่าหุ้นของ Eli Lilly จะทำหน้าที่เป็นตัวชี้วัดสำคัญ

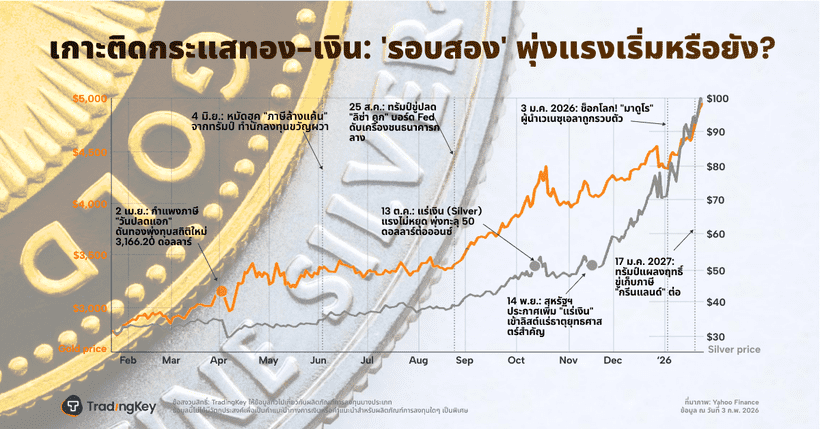

3 แผนภูมิสะท้อนภาพการเปลี่ยนแปลงของราคาทองคำและเงิน

TradingKey - ราคาทองคำและเงินฟื้นตัวขึ้นในวันพุธหลังจากถูกเทขายอย่างหนักเมื่อสัปดาห์ที่แล้ว โดยนักลงทุนในกลุ่มโลหะมีค่าดังกล่าวยังคงมีความเชื่อมั่น

ราคาทองคำและเงินฟื้นตัวอย่างแข็งแกร่ง: การฟื้นตัวในระยะสั้นหรือจุดเริ่มต้นของตลาดขาขึ้นรอบใหม่?

TradingKey - โลหะมีค่าดีดตัวกลับอย่างแข็งแกร่งหลังความผันผวนอย่างรุนแรง ในขณะที่ตลาดกำลังเผชิญกับการเลือกทิศทางที่สำคัญ หลังจากปรับตัวลดลงอย่างหนักติดต่อกันสองวัน ตลาดโลหะมีค่าได้กลับมาฟื้นตัวอย่างแข็งแกร่งในวันอังคารนี้ โดยเมื่อวันที่ 3 สัญญาซื้อขายทองคำและเงินล่วงหน้าในตลาดนิวยอร์กปิดตลาดพุ่งสูงขึ้นอย่างมีนัยสำคัญ ส่งผลให้บรรยากาศการลงทุนปรับตัวดีขึ้นอย่างเห็นได้ชัด นักลงทุนกำลังประเมินความตื่นตระหนกที่เกิดขึ้นก่อนหน้านี้จากปัจจัยทางนโยบายใหม่ และกำลังมองหาโอกาสในการเข้าซื้อเมื่อราคาอ่อนตัว (buy-the-dip) อย่างคึกคัก

VOO หุ้นเด่น: กองทุน ETF S&P 500 ของ Vanguard เปรียบเทียบกับ VUG และ QQQ สำหรับนักลงทุนระยะยาว

TradingKey - กองทุน ETF Vanguard S&P 500 (VOO) เป็นหลักทรัพย์ยอดนิยมที่นักลงทุนเลือกถือมาอย่างยาวนาน เพื่อเข้าถึงหุ้นสหรัฐฯ ในวงกว้าง เมื่อมีผู้คนหันมาลงทุนแบบ Passive และสนใจ “กองทุน ETF Vanguard ที่ดีที่สุด” มากขึ้น การถกเถียงระหว่าง VOO, กองทุน ETF Vanguard Growth (VUG) และ Invesco QQQ Trust (QQQ

SanDisk (SNDK) หุ้นยักษ์ใหญ่ Flash Memory: เจาะลึกปัจจัยหนุนการปรับตัวขึ้น และยังน่าซื้ออยู่หรือไม่?

TradingKey ยังคงมองเห็นศักยภาพการเติบโตระยะยาวของ SanDisk แต่เตือนนักลงทุนไม่ให้คาดหวังราคาหุ้นระยะสั้นที่สูงเกินไปนัก เนื่องจากอัตราการปรับขึ้นในอนาคตมีแนวโน้มชะลอตัวลงอย่างมาก ดังนั้น กลยุทธ์ที่รอบคอบกว่าคือการรอมูลค่าหุ้นมีการปรับฐาน และรอการยืนยันถึงวัฏจักรขาขึ้นของอุตสาหกรรมที่ยั่งยืนก่อนเข้าลง