2025 Is Coming: 1 Super Stock to Buy With $350 and Confidently Take Into the New Year

A new year is right around the corner, so now might be a great time for investors to examine their stock portfolios and potentially pounce on new opportunities. If 2025 is anything like 2023 and 2024, the market will be dominated by artificial intelligence (AI) stocks, so that might be a good place to start.

Duolingo (NASDAQ: DUOL) is the world's largest digital language education platform. It's using AI to create a powerful learning experience for its users, which is also driving a lucrative new revenue stream.

Duolingo stock is trading at an all-time high, but here's why it could continue climbing in 2025.

A growing portfolio of AI features

The Duolingo platform was a raging success even before AI came along. The company's mobile-first approach places interactive and gamified language lessons at the fingertips of practically anybody with a smartphone. As of the third quarter of 2024 (ended Sept. 30), Duolingo had 113.1 million monthly active users, a 36% increase from the year-ago period.

The platform also had a record 8.6 million users who were paying a monthly subscription to unlock new features and accelerate their learning, which was a 47% year-over-year jump. That's where AI comes in. Earlier this year, the company launched a new subscription tier called Duolingo Max at a higher price point than its other plans, and it introduced two AI-powered features.

Explain My Answer provides personalized feedback when users make mistakes in each lesson, and Roleplay uses a chatbot-style interface to help users practice their conversational skills. But in September, Duolingo launched a brand-new AI feature for the Max plan called Video Call. As the name suggests, users can "call" a digital avatar named Lily whenever they want to practice their vocal foreign language skills, or when they need advice on how to say certain phrases.

Duolingo's long-term goal is to create a learning experience that rivals that of a human tutor, and AI will be central to achieving it.

The Max subscription is rolling out in phases, but it's now accessible to around half of Duolingo's active user base. Over time, it could drive a much higher paid penetration and become a substantial source of revenue for the company.

Duolingo raised its revenue guidance again

Duolingo generated a record $192.6 million in revenue during Q3, a 40% increase from the year-ago period. That was above the high end of the company's forecast ($189.7 million), which prompted management to increase its guidance for the full year for the third time. Duolingo is now expected to generate up to $744 million in revenue for all of 2024.

Duolingo's strong Q3 result was especially impressive because it was accompanied by a surge in profitability. The company generated $23.3 million in net income, which was a 732% increase from the year-ago period. This proves the company doesn't have to burn truckloads of cash to generate growth at the top line.

That's because Duolingo primarily advertises through free social media posts. In fact, the company spent just $25.5 million on marketing overall in Q3, which accounted for a mere 20% of its total operating expenses of $126.8 million (marketing was actually its smallest operating cost). Still, Duolingo managed to drive an 80% increase in organic social media impressions during the quarter, which means its audience is highly engaged.

A great AI stock to take into the new year

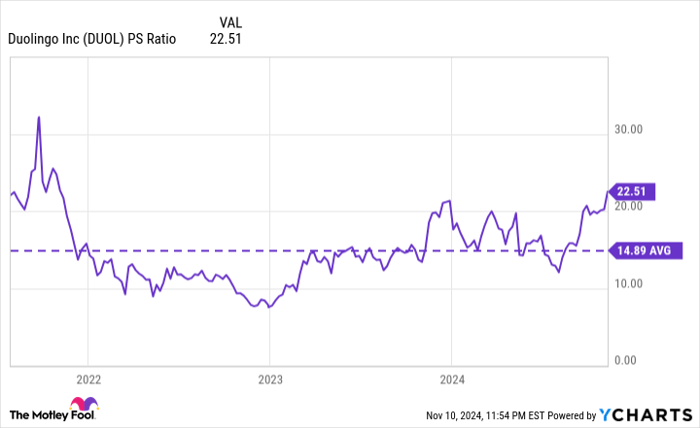

Duolingo stock isn't cheap right now. It trades at a price-to-sales (P/S) ratio of 22.5, which is a 52% premium to its average of 14.8 since it came public in 2021:

DUOL PS Ratio data by YCharts

However, the company is growing so quickly that the stock probably won't appear expensive for long. According to Wall Street's consensus estimate (provided by Yahoo!), the company could generate $959.3 million in revenue during 2025. That places it at a forward P/S ratio of 14.8, so assuming the Street's forecast is correct, the stock will be priced in line with its long-term average by the end of next year.

But here's the potential upside: The stock would have to rise by 52% throughout next year in order to maintain its current P/S ratio of 22.5, which is a real possibility, given the company's incredible growth. Plus, we know management consistently raises its revenue guidance, so Wall Street's current estimate might be too low.

Finally, more users could be enticed to buy a Max subscription as more AI features roll out, especially if they create a learning experience that rivals a human tutor, as Duolingo expects. That's a big wild card, which could drive faster revenue growth than anybody is forecasting right now.