Alibaba Earnings: What Should Chinese Tech Investors Watch?

TradingKey - For investors in China’s big technology stocks, Alibaba Group Holding Ltd (NYSE: BABA) (HKEX: 9988) is one of the most recognisable names. The e-commerce giant has amassed a loyal following and customer base given its various online retail platforms like Taobao, Tmall and Lazada.

Last year, the company also went through a leadership overhaul with Eddie Wu taking over as CEO and claiming he would be focus on getting Alibaba’s core China e-commerce business back to growth.

Alibaba has also benefitted massively from the recent China stock market rally, where its New York-listed shares soared nearly 30% in a matter of weeks.

However, a more important test of the company’s true health will come when Alibaba reports its Q2 FY2025 earnings (for the three months ending 30 September 2024). The company is set to report its latest numbers this Friday (15 November) before the market opens in the US.

For Chinese technology stock investors, here’s what they should be watching as one of the biggest Chinese companies reports its results.

Gauge of Chinese consumer strength and sales growth

Given Alibaba’s massive size – its various platforms in China count just over 1.1 billion users of its apps – the company is also a bellwether for how consumer confidence is faring in the world’s second-largest economy.

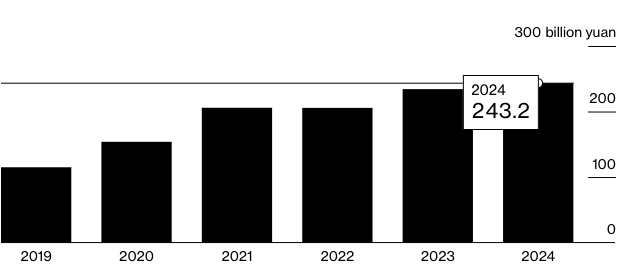

Last quarter, for Q1 FY2025, Alibaba reported extremely anaemic revenue growth of just 4% year-on-year for the period, pulling in RMB 243.2 billion (US$34 billion). Meanwhile, there was a nasty surprise hidden under the top line number as the company’s Taobao and Tmall services – its biggest retail platforms – recorded a drop of 1% in revenue.

The poor top line number saw Alibaba’s shares fall on the release of its Q1 FY2025 results in mid-August and coming into these earnings, investors will be watching whether sales growth can rebound in its core China e-commerce businesses.

Elsewhere, its international arm saw strong revenue growth of 32% year-on-year in Q1 FY2025 and this was driven by its sizeable Southeast Asia-focused business Lazada. However, losses are expected to persist in its international business.

Rising competition

Beyond that, the rising competition from the likes of Pinduoduo – PDD Holdings Inc (NASDAQ: PDD) – will be watched closely as Alibaba has lets its edge slip over the past few years compared to its nimbler rival.

There’s also JD.com Inc (NASDAQ: JDD) (HKEX: 9618) and Meituan (HKEX: 3690), which has expanded into the grocery space, that makes the e-commerce sector a crowded, and fiercely competitive, area to operate in for Alibaba. This rising competitive landscape and poor Chinese consumer sentiment generally has seen Alibaba’s revenue growth slow considerably in recent years.

Alibaba sales FY2019 – FY2024 (RMB billion)

Sources: Bloomberg, company filings

As for Alibaba’s cloud computing arm, the previous hyper-growth has slowed considerably as competition heats up from state-backed players like China Telecom and Huawei Technologies. In the latest quarter, Alibaba’s cloud unit saw 6% year-on-year revenue growth and higher uncertainty on the corporate spending front is expected to weigh on its earnings in the quarters ahead.

Focus on shareholder returns

Last quarter, investors were also looking at how Alibaba would use its considerable cash flow and whether there could be more share buybacks on the horizon. Management repurchased 613 million shares during its latest quarter for a total of US$5.8 billion.

A few months ago, Alibaba announced a further US$25 billion that would be spent on share buybacks – in addition to an already sizeable buyback plan. As of the end of June 2024, the remaining amount of money authorised by Alibaba’s board for share buybacks is US$21.6 billion.

That could provide some cheer for investors in China tech stocks, given the relatively poor growth outlook for the big players, including Alibaba. While Alibaba’s New York-listed shares are down nearly 20% from their recent high (on the back of the China rally), the company’s stock price is still up 27.6% so far in 2024.