Research on Celsius(CELH)—Representative of Energy Drink

(1).jpg)

Definition

The energy drink sector is characterized by products that contain high levels of caffeine, along with added sugars and a variety of other ingredients, such as the legal stimulants guarana, taurine, and L-carnitine. These components are designed to enhance alertness, concentration, and energy levels. Energy drinks are promoted to improve both cognitive sharpness and physical performance.

Industry Size

1)Market Value: the global energy drink market was valued at $73.81 billion in 2023 and is anticipated to exhibit a robust CAGR of 7.9% from 2024 to 2030, with an estimated market value reaching $125.11 billion by 2030.

2)Regional Distribution: the North American market held a significant share, accounting for c.37% of the global market in 2023. This demand is largely attributed to the region's fast-paced lifestyle and a growing emphasis on health and wellness. The U.S. market dominated the North American share, claiming around 85%.

3)Leading Brands: Red Bull, Monster Energy, and Celsius.

Global market size of energy drink industry

Source: Grand View Research, Tradingkey.com

Industry growth driver

We've observed that the sales growth of the energy drink industry in the US market has primarily been fueled by volume expansion in the past, while the ASP has occasionally seen declines.

Energy drink industry growth analysis

Source: Statista, Tradingkey.com

Currently, the ASP of energy drink is under pressure, as 1) the primary consumer group—blue-collar workers—are facing rising inflation and interest rate pressures, which have led to changes in their consumption habits and purchase frequency; 2) the industry is experiencing intense competition due to the continuous launch of new products and promotional activities. Additionally, the temporary dip in foot traffic at convenience stores also affects the industry's growth.

Trends and shift in the industry

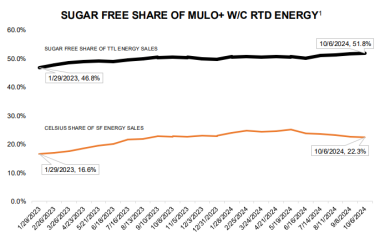

1) natural ingredients and lower sugar levels shift: In response to this, brands are launching sugar-free and calorie-free options to meet the demands, therefore, the traditional segment of full-sugar energy drinks has experienced a decline in growth in recent years, while the sugar-free category has gained momentum, now accounting for over half of the market share.

2) surge in the importance of performance among 18-34-year-olds, with 46% now prioritizing it—a 10% rise yoy.

3) female consumers: on the rise, breaking away from the market's historical concentration on young male demographics.

Sugar-free Segment Analysis in MULO+W/C Ready-to-Drink Energy Market

Source: Company data, Tradingkey.com

4) a diverse range of innovative options: these beverages are designed with distinctive flavors and specific benefits, targeting areas like cognitive enhancement, stress relief, and immune support.

Product Landscape Analysis of Leading Brands

Brand | Energy product | Picture demo | Sales for 2023 |

Red bull (Private company) | · Red bull Energy drink · Red bull Sugar free · Red bull Red Edition · Red Bull Apricot Edition · Red Bull Purple Edition | | Cans sold: 12.14 billion(+4.8% yoy) Turnover: EUR 10.55 billion(+9% yoy) |

Monster (Public company) | · Monster Energy (7 flavors) · Monster Energy ULTRA (9 flavors) · Monster Coffee+Energy (5 flavors) · Monster Punch+Energy (5 flavors) · Monster Refresh+Recover+Revive (4 flavors) | | Net sales: $7.14 billion (+ 13.1% yoy) Net income: $1.63 billion (+ 36.9% yoy) |

Celsius (Public company) | · Celsius Originals and Vibe (27 flavors) · Celsius ESSENTIALS (6 flavors) · Celsius ON-THE-GO (Energy powders) (12 flavors) | | Revenue: $1.32 billion 2023 (+ 102%) Net income attributable to common stockholders: $182.0 million (compared to a net loss of $198.8 million) |

Source: Company data, Tradingkey.com

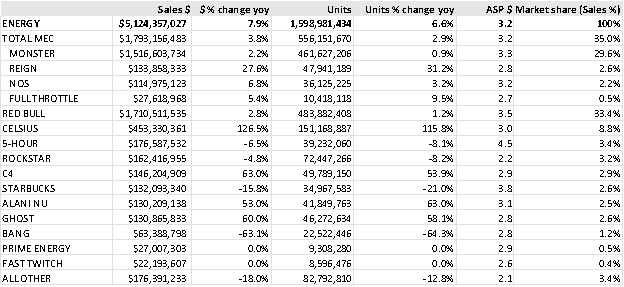

Key players in the industry

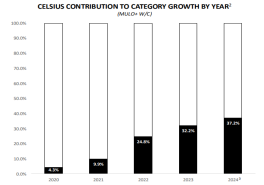

The market concentration within the energy drink industry is remarkably high, where the top three competitors—Red Bull, Monster, and Celsius—collectively command a market share of 77.2% as of the end of 2023. Celsius has shown an impressive 115.8% yoy increase in units sold, despite having an ASP below the average, significantly contributing to the expansion of the energy drink category.

Snapshot: Sales and Market Share Dynamics Among Top Brands

Source: Nielsen Total US xAOC + Conv 13 weeks ending 12/30/2023 TNA Energy, Tradingkey.com; Note: All measured channels snapshot 13wks

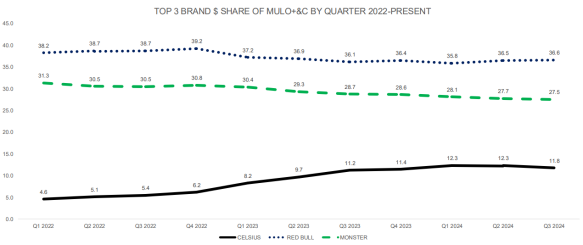

By the end of Q3 2024, Red Bull, Monster, and Celsius held market shares of 36.6%, 27.5%, and 11.8% respectively in the MULO+C channel. Notably, Celsius's market share has grown from 4.6% in Q1 2022 to 11.8% in Q3 2024, while Red Bull and Monster's market share have remained stable or declined slightly.

Top 3 brand $ share of MULO+&C by quarter 2022-present

Source: Company data, Tradingkey.com

Given that many companies in the industry are privately held, we have chosen to conduct an in-depth analysis of CELH and Monster to gain a better understanding of the sector.

Celsius

Celsius Holdings, Inc. develops, processes, markets, distributes, and sells functional energy drinks and liquid supplements in the United States, Australia, New Zealand, Canadian, European, Middle Eastern, Asia-Pacific, and internationally. The company offers CELSIUS, a fitness drink or supplement designed to accelerate metabolism and burn body fat.The company was formerly known as Vector Ventures, Inc. and changed its name to Celsius Holdings, Inc. in January 2007. Celsius Holdings, Inc. was founded in 2004 and is headquartered in Boca Raton, Florida.

Stock overview

Share Price | USD 30.01 | Listings | NYSE |

Volume | 8.27m | 52wk high/low | USD 99.62/27.78 |

Market Cap | USD 7.05bn | Revenue (2023) | USD 1.49bn |

Celsius‘ products (4 product lines)

| Product | Description |

Celsius Originals and Vibe | | · Initial 12- ounce ready-to-drink form · Offer in various flavors and carbonated and non-carbonated forms · Has all 27 flavors |

Celsius ESSENTIALS | | · Introduced in 2023 · Available in 16-ounce cans · Formulated with aminos |

Celsius ON-THE-GO (Energy powders) | | · On-the-go powder form · Features the same ingredients contained in functional energy drinks |

Source: Company data, Tradingkey.com

Celsius contribution to category growth by year

Source: Company data, Tradingkey.com

Business model

1)Celsius is involved in the development, processing, marketing, sale, and distribution of functional energy drinks. The company outsources its manufacturing to third-party co-packers and has established a network model that includes the use of co-packers and warehousing for product distribution. In Nov 2024, Celsius acquired Big Beverages for $75m (vs. Cash and cash equivalents 903m in Q3 2024) to bolster its innovation capabilities, R&D and supply chain control, with the anticipation of realizing both short- and medium-term financial benefits.

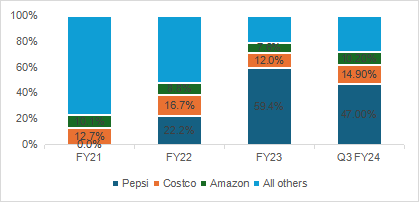

2)Distribution channels: across various domestic retail channels, including supermarkets, convenience stores, drug stores, nutritional stores, mass merchants, health clubs, gyms, military channels, and e-commerce. The company uses a hybrid distribution model with direct-store delivery (DSD) and direct-to-retailer (DTR) sales and has a strong online presence. Among its notable partners are PepsiCo, Costco, and Amazon, which contributed 59.4%, 12%, and 7.6% respectively to Celsius' 2023 revenue. PepsiCo has made a strategic investment in Celsius, holding an 8.5% stake in the form of preferred shares and help distribute Celsius worldwide.

Distributor Market Share Insights for Celsius

Source: Company data, Tradingkey.com

Business financials

Revenue

Celsius saw rapid revenue growth from 2020 to 2022, primarily driven by increasing sales volumes. In 2023, revenue soared by 101.7% to reach $1.3 billion. However, in 2Q 2024, Celsius's unit sales volume growth slowed to 30.6% yoy, with ASP down 5.6% yoy. Revenue for 3Q 2024 fell short of consensus estimates by nearly $1 million, declining to $265.7 million from $384.8 million in the previous year, a 31% reduction. This downturn indicates ongoing operational challenges, even with steady U.S. retail sales and expanding international market presence.

Revenue Analysis of Celsius

| Volume | Price | Reasons behind volume change in US market |

2019 | Primarily | —— | —— |

2020 | Primarily | —— | The primary factors:growth in e-commerce channel |

2021 | Largely attribute to | —— | 1) continued strong triple-digit growth in traditional distribution channels 2) increase in and optimization of products’ presence in world class retailers 3) the continued expansion of DSD network 4) fitness and vending channels reflected triple digit growth yoy |

2022 | Largely attribute to | —— | 1) continued strong triple-digit growth in traditional distribution channels 2) increase in and optimization of products’ presence in world class retailers 3) expansion of DSD network and transition to the PepsiCo distribution network in 4Q2022 |

2023 | Partially | —— | 1) continued gains in distribution points 2) SKUs per location improvement |

2024Q1 | Partially | —— | 1) increased consumer demand 2) continued growth in the club, e-commerce and food service channels, convenience and gas channel, etc. |

2024Q2 | +30.6% | -5.6% | 1) strength in the club, e-commerce and food service channels (solid drivers) 2) strong quarterly yoy share gains in the convenience and gas channel |

2024Q3 | —— | —— | 1) revenue from PepsiCo declined $123.9 million yoy as of inventory optimization 2) retail sales grew by 7.1% yoy |

Source: Company data, Tradingkey.com

Celsius' revenue has been significantly impacted by PepsiCo's inventory strategies. In Q1 2023, PepsiCo increased its stock of Celsius products by an estimated $20-25 million, and maintained these levels for the rest of the year. However, in 2024, with a market slowdown, PepsiCo chose not to restock in Q1, and Celsius undertook inventory optimization to keep levels within a reasonable range at this quarter. Despite these efforts, Celsius saw a substantial drop in revenue due to PepsiCo's inventory management practices Q3 2024.

Analysis of PepsiCo’s inventory impact

| PepsiCo’s inventory impact |

2022Q3 | approximately $15 million to $20 million was driven by the inventory pipe fill in third quarter(restocking) |

2023Q1 | an increase in the days inventory outstanding within the mixing centers relative to the end of 2022, which equated to roughly $20 million to $25 million in incremental sales (restocking) |

2023Q2-Q4 | across Q2 and Q3, saw some minor buildup; kind of stock steady for Q2, Q3, Q4 |

2024Q1 | revenue adversely affected due to inventory movements by PepsiCo, no restocking happened, optimization of inventory level |

2024Q2 | the impact of the inventory movements during the middle of June was c.$20-30 million, the impact was at the lower end of that range in 2Q24 |

2024Q3 | Inventory optimization of PepsiCo (around 100-120 million) (destocking) |

Source: Company data, Tradingkey.com

Due to the effects of excess inventory and inventory optimization at Pepsi, Celsius' revenue has been significantly disrupted and does not accurately reflect the actual market demand. Therefore, Celsius also monitors changes in retail sales. In Q3 2024, retail sales saw a yoy increase of 7.1% (vs yoy revenue decline of -30.9%), which could indicate that market demand for Celsius has not waned that much.

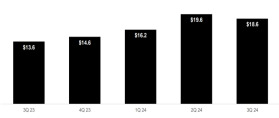

International expansion: sales surged by 37% to $18.6 million in Q3 2024, driven by strategic entries into Canada, the U.K., and Ireland. This underscores the importance of global expansion for future growth. With plans to enter Australia, New Zealand, and France in H2 2024, the company is set to further accelerate its growth. Although the U.S. market still dominates, contributing 96% of total revenue in 2023, we anticipate international revenue to gain a larger share in the near future.

Celsius' Quarterly International Revenue

Source: Company data, Tradingkey.com

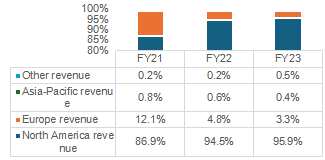

Regional Breakdown of Celsius' International Revenu

Source: Company data, Tradingkey.com

GPM(Gross Profit Margin)

We noticed an uptick in GPM since 2022, fueled by reduced costs for raw materials and freight, along with enhanced operational efficiency. Nonetheless, in Q3 2024, GPM took an unexpected dive from 50.4% to 46%. This decline was primarily attributed to supply chain disruptions, largely stemming from promotional allowances, incentives, and other billbacks originating from retail partners. Management is targeting a range in the high 40s to 50, and we are projecting an average gross profit margin of 49.2% for the entire year.

Analysis of Celsius’ gross profit margin

| change | Reasons behind gross profit margin change |

2020 | increase | mainly increases in volume |

2021 | decrease | increases in raw material costs (primarily aluminum cans), ocean freight costs, distribution costs, repackaging costs and processing costs (all directly related to added complexities in the supply chain because of the COVID-19 pandemic) |

2022 | increase | 1) ability to leverage the increased volumes 2) increased pricing and improved processes and freight lanes 3) offset in part by increases in raw material costs (including high priced aluminum cans that were significantly depleted throughout 2022) |

2023 | increase | 1) efficiencies in raw material sourcing 2) product waste reduction |

2024Q1 | increase | reduced freight and raw material costs |

2024Q2 | increase | reduced raw material costs and freight costs |

2024Q3 | decrease | due to promotional allowances, incentives, and other billbacks, which are from retail |

Source: Company data, Tradingkey.com

Expense

1)effective expense management: with the G&A expense ratio falling from c.18.3% in 2021 to c.8.0% in 2023, reflecting improved operational efficiency.

2)the selling and marketing expense ratio fluctuated from 2021 to 2023: a decline from c.23.8% in 2021 to c.20.4% in 2023, suggesting more impactful marketing investments. In 2022, there was a notable increase in sales and marketing expenses, mainly due to termination fees and trade-marketing activities amounting to $196.3 million. The management's ongoing investment in marketing and sales is strategic and growth-focused, with the expectation that the increased revenue will compensate for the higher expenses, maintaining a strong financial equilibrium.

stock price review

Between 2020 and early 2024, Celsius witnessed a significant surge in its stock value, primarily due to the company's robust product offerings and successful channel expansion strategies, which led to higher revenues and an expanded market share. The market held positive expectations for the company during this period. However, the stock has plummeted 45.0% year-to-date and is down 68.8% from its peak, primarily due to pressures in the functional beverage industry—declining consumption frequency among blue-collar workers amidst inflation, and promotional pressures stemming from inventory buildup at the company's main supplier, PepsiCo.

Share price of Celsius:

Source: Google Finance, Tradingkey.com

Peer comparison-Monster

Monster is a leading player in the energy drink market, ranking second in the U.S. behind Red Bull.

Revenue of Monster

Segment Name | 2023 revenue $ | Content | |

Monster Energy Drinks | 6,555,089 | Primarily comprised of Monster Energy drinks, Reign Total Body Fuel high performance energy drinks, Reign Storm total wellness energy drinks, Bang Energy drinks, and Monster Tour Water. | |

Strategic Brands | 376,589 | Primarily comprised of various energy drink brands acquired from Coca-Cola in 2015, as well as affordable energy brands Predator and Fury. | |

Alcohol Brands | 184,855 | Comprised of various craft beers, hard seltzers, and FMBs. | |

Other | 23,494 | Comprised of certain products sold by AFF. | |

Source: Company data, Tradingkey.com

strategic alliance with TCCC: Since 2008, Monster has utilized TCCC's extensive distribution network to enhance its global presence. The partnership deepened in 2014 with TCCC's 16.7% investment in Monster, accompanied by an exchange of the companies' energy and non-energy beverage portfolios. This collaboration has propelled Monster Energy's international expansion, leading to a substantial growth in its foreign sales.

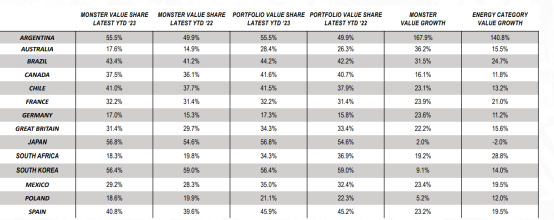

Monster’s revenue from different regions:

Source: Nielsen data, Tradingkey.com; date as of end 2023

Monster's YTD stock return stands at -5.0%, and it is currently trading at a P/E (TTM) ratio of 33.65x. When compared to its historical average P/E ratio over the past five years, which was 44.39x, Monster appears to be trading at a lower valuation than its historical norm.

Share price of Monster

Source: Google Finance, Tradingkey.com

Our view for Celsius: Hold

Valuation: Celsius is currently trading at a trailing twelve-month (TTM) P/E ratio of 41.22x, which exceeds Monster's P/E ratio of 33.65x. However, looking ahead to 2025, the forward P/E ratios for Monster and Celsius are anticipated to be 32.58x and 42.0x, respectively. We do not expect Celsius's earnings growth to surpass Monster's, given the many headwinds Celsius is currently facing due to intensifying market competition, and there’s minimal market share fluctuation between Monster and Celsius year-to-date. This suggests that, despite a significant drop in its stock price, Celsius is still considered overvalued. We are inclined to wait for the previous valuation bubble to be fully absorbed before making any investment decisions.

Market dynamics: Celsius is grappling with several challenges amidst a slowing industry growth rate, fluctuating blue-collar consumer preferences influenced by weak macroeconomic conditions, and aggressive competition from rivals who are consistently launching new products. Also inventory problems with Pepsi still exist.

Channel expansion: Celsius is exploring international markets, yet its foreign revenue is negligible and comes with inherent risks. Moreover, with the industry facing headwinds, the pace of global expansion could potentially decelerate.

However, we still believe Celsius boasts a strong fundamental profile for several key reasons: 1) Product Positioning: Celsius' products are well-aligned with the shifting consumer habits, catering to health-conscious preferences. 2) Customer Base: The company has a broad and diverse customer base, which provides a solid foundation for market penetration. 3) Channel Penetration: Celsius continues to expand its reach through continuous channel development, ensuring its products are available to a wider customer. 4) Partnership with PepsiCo: The strengthened relationship with PepsiCo is a key driver for revenue growth, leveraging PepsiCo's extensive distribution network. Though it faces some supply disruption currently, we believe it would benefit Celsius in the long run. Additionally, Celsius is also set to improve its financial margins by reducing raw material costs and increasing operational efficiency. The company's diverse product lineup effectively spreads risk across different market segments. Therefore, we maintain a neutral stance on Celsius.

Therefore, we believe the reasonable price for Celsius should be around $30-36.5 for FY25F, and we remain our neutral view on it.