Exchange rate outlook: Bullish on USD and bearish on EUR

Three-month view

USD index

EUR/USD

USD/CNY

USD/JPY

1. USD index

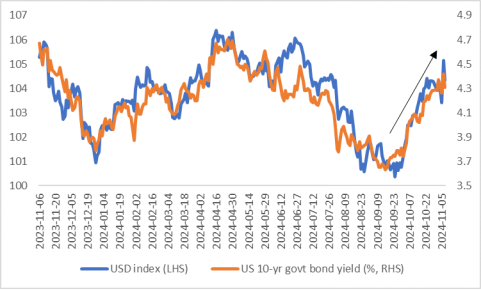

Together with US bond yields, the dollar has risen sharply since late September, rebounding from the low of 100.24 (Figure 1.1). Three factors that drove the strong performance of the dollar in October are as follows:

First, from June to September, the exchange rate market was dominated by the expectation of the Fed's interest rate cuts, resulting in the dollar being undervalued. After the Fed cut its rate by 50bp at the end of September, the undervalued currency began to correct.

Second, the tones of Fed officials in October were generally hawkish and the officials showed caution about the future path of interest rate cuts.

Third, one to two months before the election, Trump was gradually reversing and consolidating his poll advantage in the swing states. The market began to price in Trump's winning in advance.

Figure 1.1: USD index vs. US 10-year government bond yield

Source: Fed, Tradingkey.com

Appreciation: “Trump Trade”; re-inflation expectations(wage increase caused by immigrants policies and stricter tariff);pressure on Fed’s easing policy ;

Depreciation: Trump's policy aims to reduce the US trade deficit and support exports.

Therefore, the dollar may appreciate in the short term but may be under pressure in the longer term.

Macro-economics overview and influence on dollar

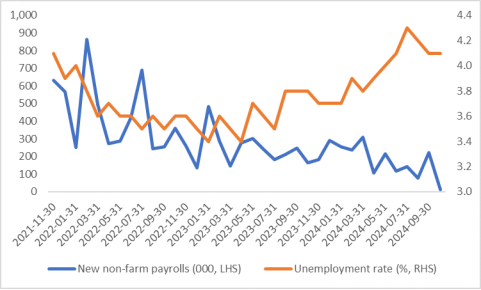

1)sluggish labour market: Affected by hurricanes and strikes, only 12,000 new non-farm jobs were added in October, significantly lower than the consensus forecast of 100,000 (Figure 1.3).

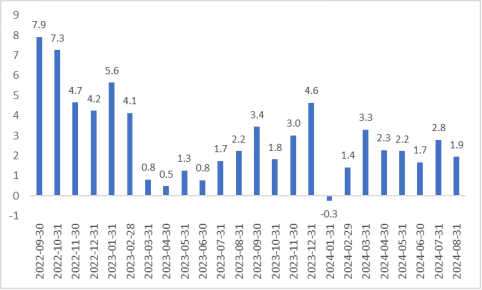

2)strong retail sales: Despite the weakening labour market, retail sales recorded positive growth for seven consecutive months (Figure 1.3).

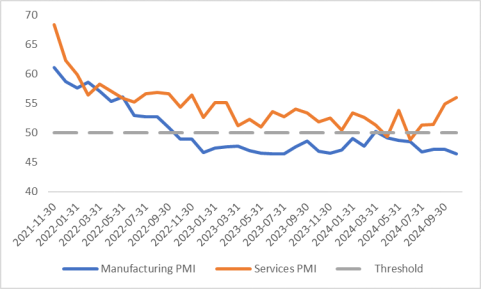

3)PMI: While the manufacturing PMI in October was 46.5, below the threshold of 50, the services industry PMI, which accounts for around 80% of GDP, was 56. This was significantly higher than the expected 53.8, and 54.9 in September (Figure 1.4). Driven by the recovery of domestic demand in the US, the new business sub-index of the PMI climbed to its highest level since April 2022.

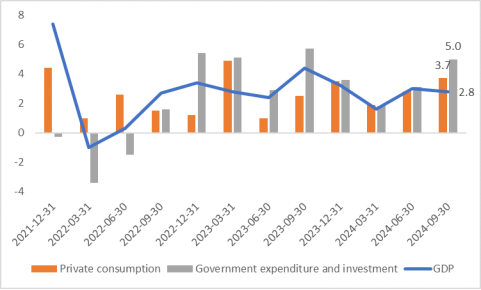

4)GDP growth: According to the data published by the US Department of Commerce on 30 October, GDP growth was 2.8% on the annualized quarter-on-quarter basis and 2.7% year-on-year in Q3 2024. From a structural perspective, the contribution of private consumption to the US economy has further increased, and government expenditure and investment have rebounded (Figure 1.5).

5)US economy: resilient.

Additionally, Fed officials have been now more hawkish, advocating gradual and prudent interest rate cuts. This may also continue to drive the dollar up in the short term.

Aside from economics, the recent escalation of geopolitical tensions has made investors more concerned about the uncertainty and headwinds of the global economic recovery. The risk aversion sentiment is also likely to increase the value of dollar as the “safe-haven” currency.

In summary, our baseline view for the USD index is bullish in the short term (3 months) and bearish in the medium term (12 months).

Figure 1.2: US labour market

Source: US Department of Labor, Tradingkey.com

Figure 1.3: US retail sales (y-o-y %)

Source: US Census Bureau, Tradingkey.com

Figure 1.4: US PMI

Source: Institute for Supply Management, Tradingkey.com

Figure 1.5: US GDP growth (annualized, q-o-q, %)

Source: US Department of Commerce, Tradingkey.com

2. EUR/USD

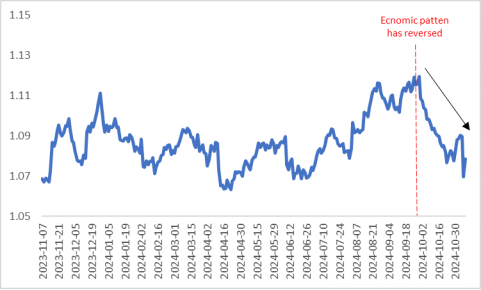

The economic pattern of accelerating the decline in inflation and recession expectations has reversed since September (Figure 2.1). With the resilience of US growth, the continuous publishing of inflation data of major countries and the end of the US election, the exchange rate market has begun to trade along three new mainstreams: The first is the divergence of growth between the US and the eurozone. The second is the different speeds of inflation decline in the two economies; The third is the so-called “Trump Effects”.

Figure 2.1: EUR/USD

Source: ECB, Tradingkey.com

The main reason behind the decline of the EUR/USD : weak fundamentals

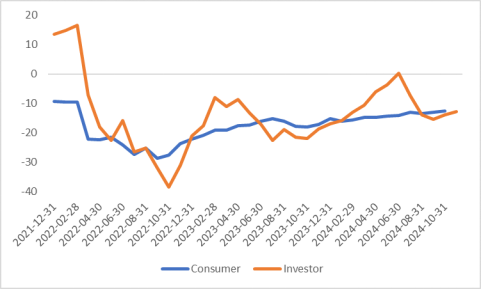

1)CPI:The eurozone consumer confidence and investors’ indices have continued to record negative growth (Figure 2.2), which worries the exchange rate market.

2)PMI:The eurozone's manufacturing PMI was 45.9 in October, still in the contracting range. While the services industry recorded a PMI of 51.2, which was above the threshold of 50, the figure was lower than the expected value of 51.5 and 51.4 in September.

3)Germany and France: once the growth engine of the Eurozone economy, Germany may fall into recession, and France has been downgraded or turned to a negative outlook by rating agencies.

In contrast, the US economy has performed strongly and its leading positions in artificial intelligence, semiconductors and commercial aerospace have continued to expand. US financial markets have continued to prosper, leading the wealth effect to offset the negative impact of the excess savings depletion.

Figure 2.2: Consumer confidence index vs. Investors' confidence index

Source: Eurostat, Sentix, Tradingkey.com

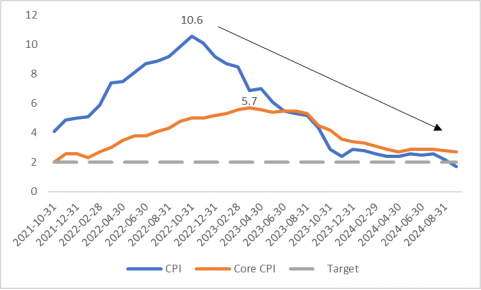

In terms of inflation, the Eurozone CPI and core CPI decreased to 1.7% and 2.7% respectively in September (Figure 2.3). Service prices also continued to decline.

Figure 2.3: Eurozone inflation (%)

Source: OECD, Tradingkey.com

In terms of the new US presidency, Eurozone countries are wary of US trade policies, especially taking into account their weak growth prospects. Looking forward, Trump is expected to introduce more radical measures on tariffs. In addition, Trump may force the EU to follow the US policy against China and urge the EU to decouple from China. Moreover, he may build bilateral relations with individual member states above relations with the EU. Under Trump's support, the Eurosceptic faction is likely to increase, exacerbating the political division tendency within the eurozone. All these factors may cause the euro to underperform. The short-term sharp drop in the EUR/USD after 8 November 2016 shown in Figure 2.5 is proof.

All in all, the above growth, inflation and the new US presidency all point to the depreciation of the EUR/USD within the next three months.

3. USD/CNY

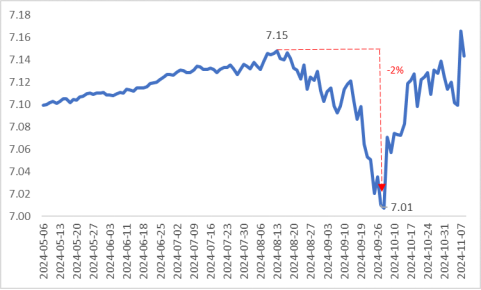

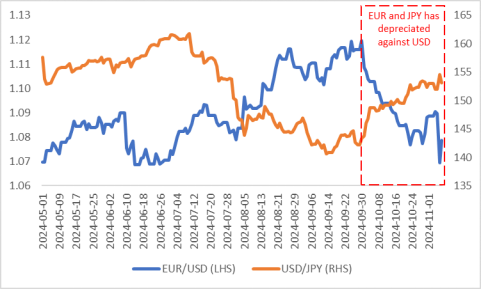

The USD/CNY fell from 7.15 in Middle August to 7.01 in late September, a drop of 2%. Recently, the logic of trading US assets has switched from rate-cut expectations to re-inflation, which has led to the appreciation of the USD/CNY since the end of September (Figure 3.1). Meanwhile, other non-US currencies such as the euro and the yen have also weakened during this period (Figure 3.2). This means the main driving force behind this round of the yuan’s depreciation comes from external factors rather than internal. Looking forward, while Trump and his policy propositions may continue to put pressure on the yuan, the pressure is expected to be limited.

Figure 3.1: USD/CNY

Source: China State Administration of Foreign Exchange, Tradingkey.com

Figure 3.2: EUR/USD and USD/JPY

Source: ECB, XE, Tradingkey.com

Key reasons supporting CNY:

1)China’s large scale stimulus : have positive impacts on cross-border capital inflows.

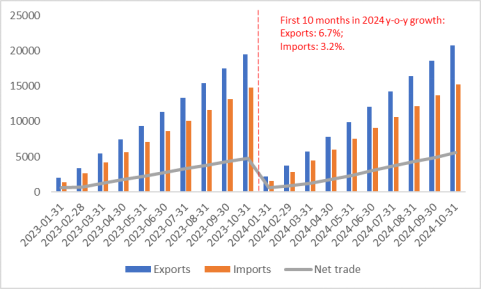

2)Trade surplus: on 7 November, the General Administration of Customs of China announced the total value of China's import and export of goods was 36.02 trillion yuan in the first 10 months of this year. Exports were 20.8 trillion yuan, up 6.7% y-o-y and imports were 15.22 trillion yuan, up 3.2% (Figure 3.6). Higher growth of exports means an increase in trade surplus, which in turn supports the yuan.

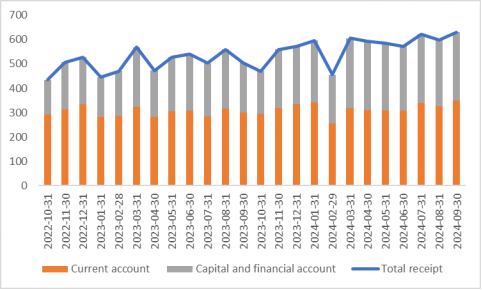

Figure 3.3: China cross-border receipts by non-banking sectors (USD billion)

Source: China State Administration of Foreign Exchange, Tradingkey.com

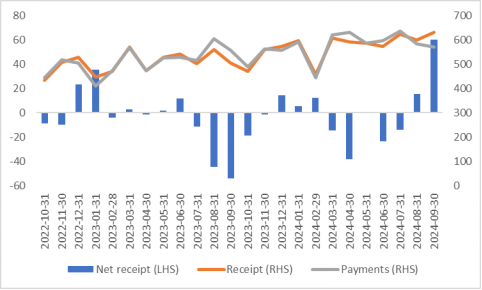

Figure 3.4: China net cross-border receipts by non-banking sectors (USD billion)

Source: China State Administration of Foreign Exchange, Tradingkey.com

Figure 3.5: China's cumulative value of imports and exports

Source: China General Administration of Customs, Tradingkey.com

Credit Risk(USD): The disorderly expansion of the US fiscal policy has led to doubts about the creditability of the dollar. Central banks have continued an increase in holding gold, driving up gold prices. This may reflect the demand for the reconstruction of the global credit system.

In conclusion, we expect both the yuan and the dollar to strengthen against other currencies such as the euro. The USD/CNY may fluctuate in the range of 7.1-7.2 within the next three months, with little possibility to break through 7.3. On the contrary, in the medium term, when the impact of the "Trump Trade" fades and the expectation of the yuan depreciation corrects, the increase in foreign exchange settlement and trade surplus may drive up the yuan.

4. USD/JPY

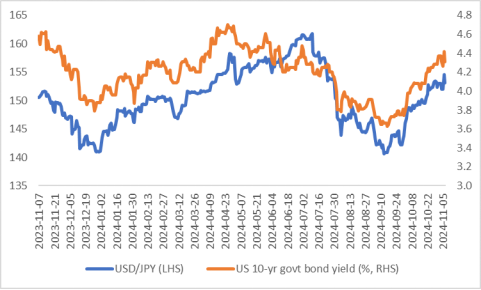

In October, due to the improvement in the US economic fundamentals rebounded, the prevalence of the pre-election "Trump Trade" and the rise in 10-year US Treasury bond yields, the USD/JPY exchange rate rose sharply (Figure 4.1).

Figure 4.1: USD/JPY vs. US 10-year government bond yield

Source: XE, Fed, Tradingkey.com

Looking forward, the price of the yen will be affected by positive and negative factors, which may offset each other.

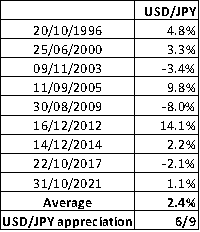

1)Historical influence: Generally, after the results of the House of Representatives election were announced, the yen was more likely to weaken in the short term. In the past 30 years, Japan held a total number of 9 House of Representatives elections (excluding the 2024 election). Three months after the elections, the USD/JPY rose 6 out of 9 times, with an average increase of 2.4% (Figure 4.2). Conventionally, the elections of the House of Representatives in Japan were usually caused by the inauguration of a new prime minister to dissolute the original House of Representatives, followed by a re-election. The main reason for the depreciation of the yen was the new Japanese government usually promised a series of policies to boost the economy. As the market's risk appetite increased, the yen, as a safe-haven currency, usually weakened. From the history lessons, the 2024 House of Representatives election may have started to put depreciation pressure on the yen.

Figure 4.2: USD/JPY 3 months after House of Representatives elections

Source: XE, Tradingkey.com

2)Political compromise between parties: likely to lead Shigeru's hawkish stance to be moderate, which may hinder the appreciation of the yen.

3)The Bank of Japan's (BoJ) Monetary Policy : the latest meeting gave a hawkish signal on 31 October. The BoJ kept its policy rates unchanged at this meeting, which was in line with market expectations. The central bank raised its forecasts for real GDP in Fiscal Year 2025 and Core CPI less fresh food and energy in Fiscal Year 2024 (Figure 4.3). In addition, Governor Kazuo Ueda signalled rate hikes at the press conference. For example, the weakening of the yen is more likely to trigger a rate hike decision; The changes in Japan's political arena will not hinder the central bank's interest rate decision; The central bank needs to clear obstacles for the financial markets to return to rationality; The resilience of the US economy will create larger space for the BoJ to raise its interest rates. Based on the BoJ's statement, we expect the next rate hike to take place in December, which may drive the yen to appreciate.

As the above-mentioned Japanese economic conditions and policies have a two-way impact on the yen, we expect the USD/JPY to fluctuate around the current level within the next three months.