Commodities Outlook: Macroeconomic policies will improve commodity demand

Gold: Watch for higher volatility

Short-term views:

Since the beginning of October, as the market's expectations of a Trump victory and a Republican sweep have heated up, investors have flocked to precious metals to hedge against U.S. fiscal deficit, inflation concerns, and geopolitical tensions. This has already been fully priced in, with gold accumulating a 35% increase since the beginning of this year. After the election, without any further positive news, a slowdown in central bank gold purchases, and the strength of the U.S. economy putting pressure on gold, the profit-taking from the "Trump trade" will emerge, leading to increased volatility in gold. Prepare for a period of choppy trading that could last for several weeks.

Long-term views:

Trump's massive spending plan will further exacerbate the pressure on U.S. public finances and increase inflation, which has been analyzed in detail in previous articles. In the long term, gold still benefits from the Federal Reserve's interest rate cuts, the depreciation of the dollar, and global central bank purchases. Gold price pullbacks are buying opportunities. Bulls should remain cautious and can use the previous low of 2600 as support, looking to go long around this price level.

Detailed factors are as follows:

1)Real interest rate: uncertain when the negative correlation between gold and real interest rates will reemerge.

The effectiveness of the traditional gold analysis framework based on real interest rates has significantly declined since 2022, with even instances of U.S. treasuries and gold moving in the same direction.

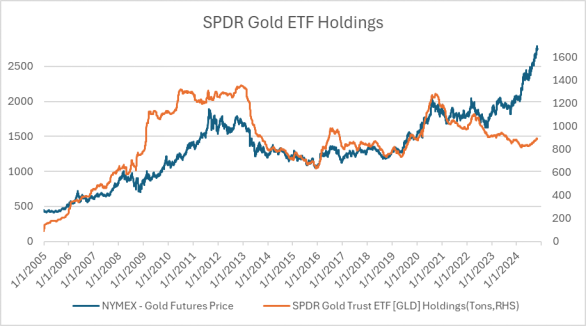

It is worth noting that the holding of gold ETFs has been recovering for three consecutive months. As the cycle of interest rate cuts begins, the investment demand for gold from the private sector is returning

2)US Dollar: Credit and Solvency of the US Government

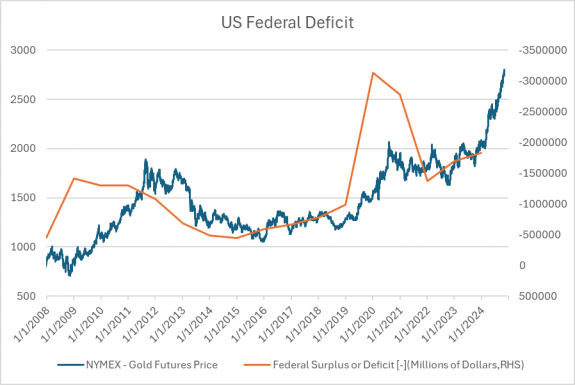

The credit risk of the US dollar is the inherent logic behind the gold price. When the credit risk of the US dollar rises, the demand for gold also increases. Furthermore, the credit of US dollar is closed related to the solvency of the US debt, leading the trend of gold prices very often.

According to a recent analysis by the Committee for a Responsible Federal Budget, Trump's policy agenda could increase the national debt by $7.5 trillion over a decade. As long as US debt continues to expand, gold will maintain its support.

Source: Reuters

However, what we may be facing is a macro situation where the US economy experiences no landing. Currently, the US Manufacturing PMI is still low. If the endogenous growth of the US economy start up in the future, the necessity for fiscal expansion may decrease, and gold price could face a period of correction.

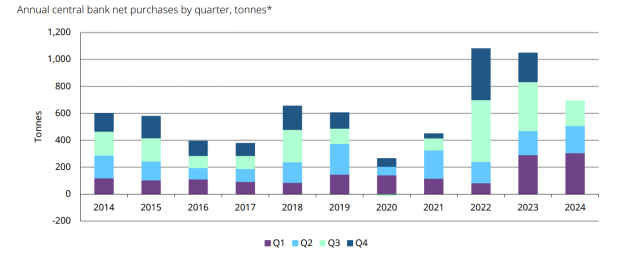

3)Central Bank Demand

Fed: The Federal Reserve began to slow down its balance sheet reduction in June, which can be seen as a de facto expansion of its balance sheet, providing support for gold prices.

Other Central Banks:

Q3: demand slowing down due to the significant rise in gold prices.

Purchasing demand: still strong(desire to increase LT allocation).

Specially, the People's Bank of China, previously the largest buyer of gold, has not increased its gold reserves for four consecutive months.

Source: World Gold Council

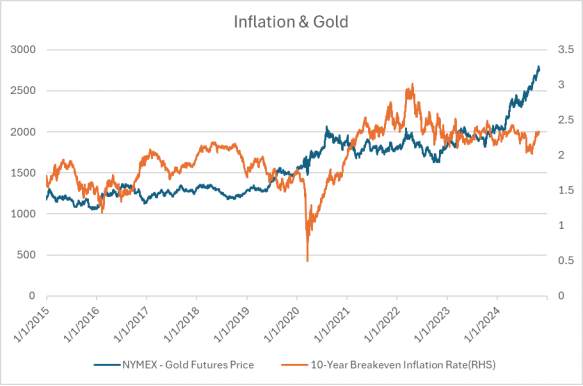

4)Inflation: gold as a good asset for hedging against inflation

Source: Reuters

According to Trump's plan, whether it's increasing tariffs or deporting a million illegal immigrants, it will cause a significant rise in US inflation. At that time, whether the Federal Reserve can raise interest rates again to curb inflation, and the impact on the market, will be a complex situation.

5)Hedge Fund Positions:

Recently, the non-commercial net long position in gold has declined, and market sentiment for a bull run in gold has been cooling down.

Source: Reuters

Crude Oil: Don’t be overly bearish and be alert to the emergence of the positives.

Short-term:

1)OPEC: delay its production increase plan --- support crude oil prices. The low level of crude oil inventories, which is close to the five-year low, has not been reflected in the market. 2)Possible Rebound: $70 is an important support level, and when prices have fallen to this level, a significant rebound has occurred a few times. Short positions are concentrated, and it would require significant momentum to drive prices even lower. If there is positive news, the rebound caused by short positions being closed could be rapid and strong.

Long-term:

1)Solid Supply: U.S. crude oil production remains high, and global supply is still accumulating. The fundamental outlook for crude oil is still weak.

2)Demand: Although demand is still weak, the global monetary easing may drive a recovery in global oil demand.

3)Geopolitics: There is also the possibility of the Middle East situation escalating again. The foreign policy of the Trump administration may have an impact on the situation in the Middle East and Russia-Ukraine.

After the election, with Trump's victory, there is a possibility of sanctions being imposed on Iran, so the market should be cautious of sudden changes. In 2018, the maximum pressure sanctions reduced Iran's crude oil production to 2 million barrels per day. For Russia, there is a possibility of lifting the $60 export oil price cap in exchange for a ceasefire, as the existing price cap policy benefits China and India.

Detailed factors are as follows:

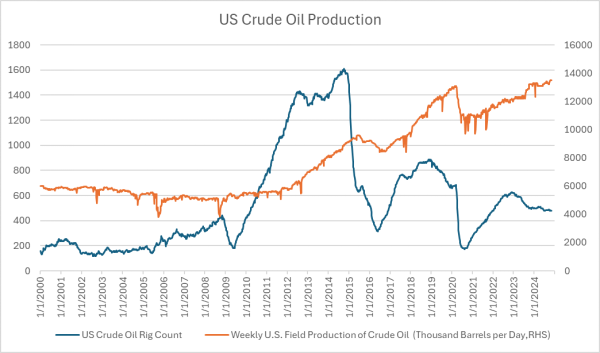

1)Supply from US:

Oil production trend: continuously climbing.

Production growth contributors: Texas and New Mexico.

Nevertheless, as the world's largest oil-producing country, its growth trajectory has had a significant impact on the market, with a general expectation of oversupply next year.

Source: Reuters

Thanks to improved efficiency, energy companies can still profit from it, so there is no incentive for American energy companies to reduce production for now. The break-even prices to profitably drill range from $59 to $70 per barrel, according to the Dallas Fed Energy Survey. Although Trump encourage more production, if price drops below break-even price, oil companies will not want to increase their losses.

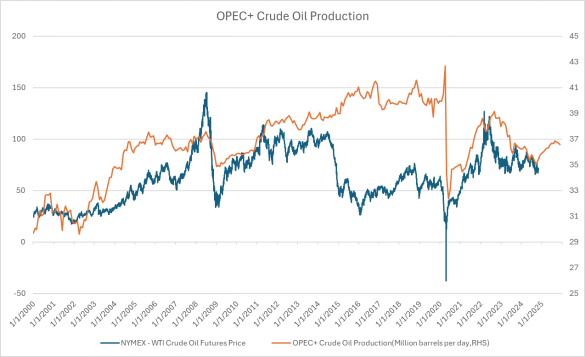

2) Supply from OPEC:

OPEC has postponed its planned increase in oil production for December. This decision comes in response to pressure on oil prices due to weak demand and the expansion of supply in the Americas. Even if the OPEC+ does not increase supply, the global market will still face an oversupply situation next year. Currently, OPEC+ has cut crude oil production by 5.86 million barrels per day, which is about 5.7% of global oil demand.

Source: Reuters

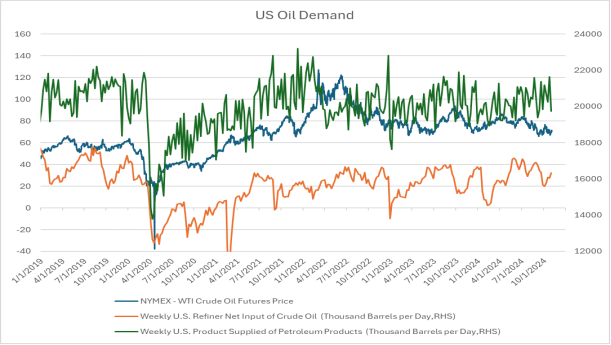

3)Demand:

The crude oil demand in China and the United States remains relatively weak. Last week, the daily crude oil processing volume of U.S. refineries was 16.3 million barrels, an increase of 281,000 barrels per day from the previous week; the Utilization of Refinery Operable Capacity of U.S. refineries last week was 90.5%, higher than the previous week's 89.1%; the total demand for petroleum products in the United States was 19.739 million barrels per day, down by 1.899 million barrels.

Source: Reuters

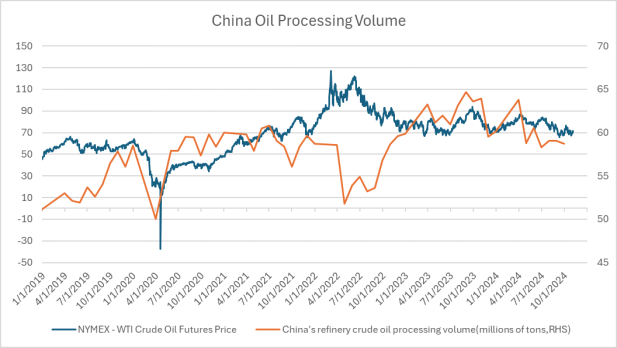

China's crude oil processing has decreased. In September, the crude oil processing volume of industries above scale was 58.73 million tons, a year-on-year decrease of 5.4%; with an average daily processing of 1.958 million tons. From January to September, the crude oil processing volume of industries above scale was 531.26 million tons, a year-on-year decrease of 1.6%.

Source: Reuters

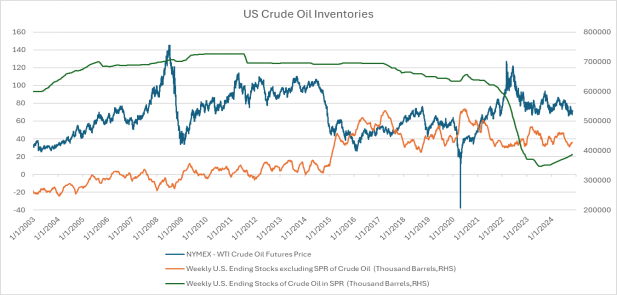

4)Inventory:

EIA shows that the inventories of crude oil, gasoline, and distillate fuels in the United States all increased last week, but still low compared to last five years. U.S. EIA crude oil inventories increased by 2.149 million barrels to 428 million barrels in the week ending November 1, an increase of 0.51%.

Source: Reuters

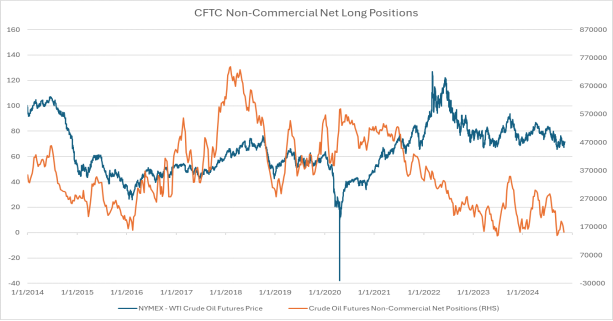

5)Hedge Fund Positions:Crude oil speculative net long positions continue to decline to nearly a ten-year low.

Source: Reuters

Copper: The recent economic stimulus measures in China are taking effect.

Short-term: Fluctuates with macro polices of China and U.S

Long-term:

1)Positive: the loose monetary and fiscal policies of both the United States and China;

recovering copper demand from China's real estate industry(stimulus policies).

2)Negative: Trump's tariffs have a significant impact on certain sectors of the copper end-products industry, such as home appliances and electronic devices, which are manufactured in China. This may affect the exports of some copper-end products to the United States, thereby impacting the copper consumption market.