Intel Corp CEO Steps Down With Shares Declining 50% in 2024. Here’s What Investors Need to Know

TradingKey - In the world of semiconductors, one big company has been a key part of the industry for decades; Intel Corporation (NASDAQ: INTC). It was founded in 1968 by chip pioneers Robert Noyce and Gordon Moore – after which “Moore’s Law” is named.

It has had decades of success, from working with Microsoft Corporation (NASDAQ: MSFT) to create a formidable partnership in PC microprocessors in the 1990s to working with Apple Inc (NASDAQ: AAPL) on chips for their smartphones and Mac laptops.

However, more recently, the company has run into trouble and on Monday (2 December) it was announced that Intel CEO Pat Gelsinger would be retiring from his role, effective immediately. With the Intel share price down 50% so far in 2024, it’s not exactly a surprise.

Intel’s share price initially reacted positively to the news of Gelsinger’s resignation and was as high as 5.5% during Monday trading but eventually ended the day down 0.5%, a sign of just how challenging taking over the company will be.

But here’s what investors need to know about Gelsinger’s resignation and how Intel plans to bounce back from its current predicament.

Gelsinger fails to impress as CEO

Gelsinger took over Intel CEO in 2021 and actually began his career at Intel in 1979. He broke that tenor up by serving as CEO of VMWare from 2012 before returning to Intel in the top job nine years later.

He took over the role based on a turnaround plan that would see Intel compete meaningfully in the “foundry” space of semiconductors by spinning off its in-house manufacturing capabilities. That would allow it to serve fabless customers without any conflict of interest, an issue that had driven many customers towards the leading foundry, Taiwan Semiconductor Manufacturing Co Ltd (NYSE: TSM) – also known as TSMC.

Over the past decade, TSMC has taken an unassailable lead in the foundry space of the chips business by focusing solely on manufacturing chips for semiconductor designers such as Nvidia Corp (NASDAQ: NVDA).

As a result, Intel fell behind given its attempt to be both a designer and foundry player – what’s termed an integrated device manufacturer (IDM). However, that model has proven much less lucrative than either being a pure-play foundry (like TSMC) or a pure-play fabless designer, like Nvidia or Broadcom Inc (NASDAQ: AVGO).

But it’s been in the Artificial Intelligence (AI) space that Intel has really been found wanting. Both Nvidia, which dominates AI, and Advanced Micro Devices (NASDAQ: AMD) – also known as AMD – have turned the AI chip space into a “two-horse race”.

Since Gelsinger took over a CEO of Intel in February 2021 to his resignation on 1 December 2024, Intel shares have lost over 60% of their value. It suspended its dividend in August and in August 2023 cut its dividend by 65%.

Intel business in trouble

Intel’s latest Q3 2024 earnings highlight the issues the permanent incoming CEO will have to deal with. During the quarter, Intel posted revenue of US$13.3 billion, which was down 6% year-on-year from the same period a year ago.

It recognised around US$2.8 billion of “restructuring charges” during the period which related to the US$10 billion cost reduction plan that Gelsinger had announced that would run into 2025. Its non-GAAP gross margin of 18.0% was down a whopping 27.8 percentage points from the 48.5% gross margin recorded in Q3 2023.

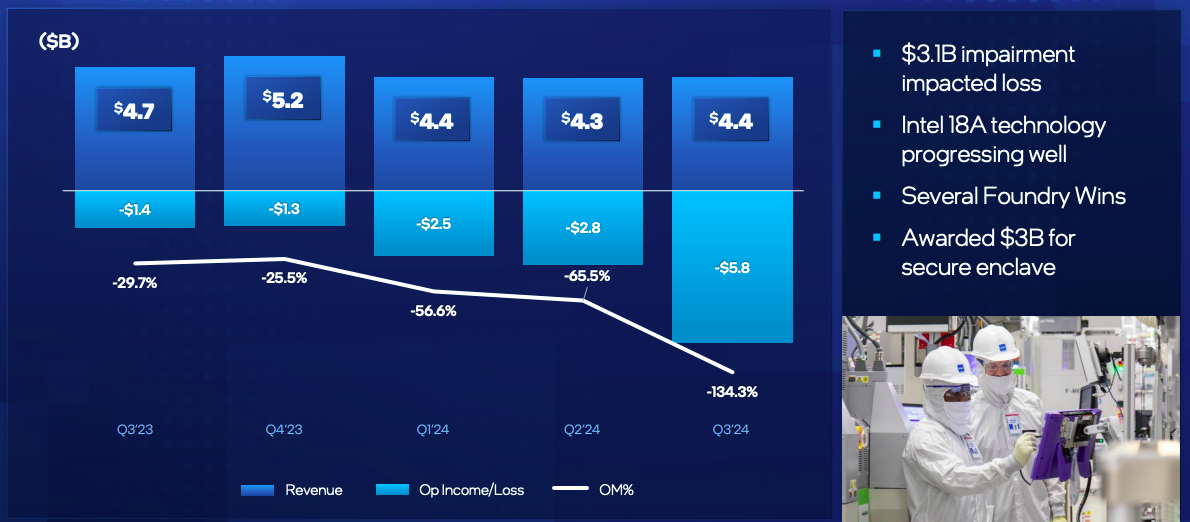

On the foundry side, the business remained stagnant in the latest quarter with revenue of just US$4.4 billion, down significantly from the US$4.7 billion recorded in Q3 2023. The unit’s operating loss ballooned to US$5.8 billion on a sizeable impairment loss.

Intel foundry revenue, operating loss (US$ billions) and operating margin (%)

Source: Intel Q3 2024 earnings presentation

Meanwhile, Intel’s Q2 revenue of US$12.8 billion was down 1% year-on-year, meaning the latest set of results saw an acceleration in that rate of revenue decline – not something the Intel board probably appreciated.

Despite being one of the biggest beneficiaries of funding from the US CHIPS and Science Act, Intel hasn’t been able to capitalise on government support to build out its foundry capabilities meaningfully.

That probably has to do with the enormous capital expenditures required as well as the well-publicised delays to the construction of Intel fab plants, both in the US and Germany.

Where do Intel shares go from here?

How Intel’s share price fares from here may depend on who’s appointed and how much time they’re given. However, with the gulf between Intel and Nvidia/AMD only growing in the AI design space – and TSMC continuing to dominate the foundry sector – it’s difficult to see how a turnaround plan will take less than 5-10 years to implement.

For now, Intel CFO David Zinsner and Intel Products CEO MJ Holthaus have been named as interim co-CEOs. It’s not likely an arrangement which will be made permanent. With such a dire outlook for the company, it may proceed to hire an outsider to shake up strategy and deliver a successful turnaround plan.

Yet the jump in Intel’s share price on Monday, and then subsequent pullback, highlights just how difficult the market thinks that will be for the eventual new CEO.

.jpg)